The message from many financial advisers is that to be successful, investing must be complicated. Sorting through hundreds of investments to come up with the "best" choices and then constantly tweaking your holdings to reflect every new stock that comes along is not only impractical, it also reinforces the myth that one needs to pay someone high fees to manage the process. The fact is that the more complicated your investing strategy and the more investments you accumulate; the harder it will be to monitor your portfolio and the more things that can go wrong.

According to a recent BNY Mellon survey, more than 20% of those under 30 said they received no financial guidance at work or during school. It is not a surprise that more than 50% of those surveyed admitted that they did not know how much they would need to save for retirement. Below is how we suggest getting started.

1. You don’t need to be wealthy to invest, but you need to invest to be wealthy

One of the biggest financial advantages out there is something anyone can access by opening a simple investment account. This is the mathematical magic of compound interest. Albert Einstein called it the eighth wonder of the world for good reason.

Start by opening a retirement account, such as an IRA, that can be set up by individuals. These aren't just savings accounts; they can be used to actively invest. The taxes incurred by traditional IRA accounts on gains and dividends are deferred until retirement date when you withdraw. The below graph from US News and World Report, dated Oct. 19, 2015, shows just how powerful compounding can be.

The blue top line shows that if Susan, who is 25, invests $250 a month early in her career, she is well on her way to being a millionaire by age 65 if you assume a 7.5% return. The red line shows the savings growth, net of fees, which could cost as much as $150,000. The purple line shows that one would only have just over $100,000 if they put their money in a basic savings account.

2. When you start saving is more important than how much you save

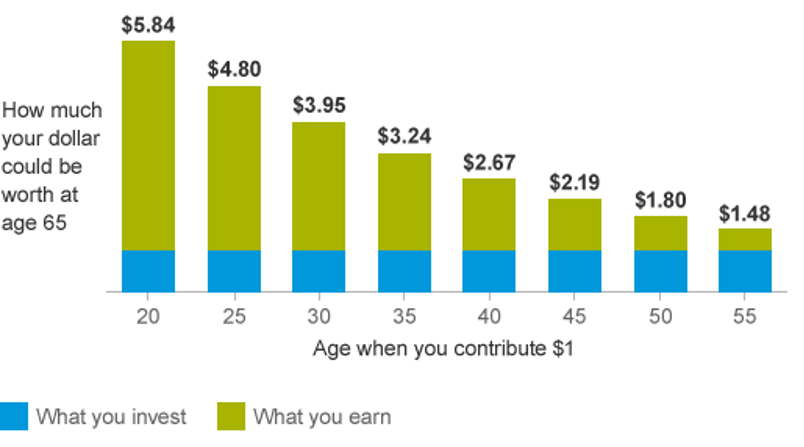

Even with volatile swings in the market, investing when you’re young and for the long haul is more fruitful than letting your money sit in a savings account. In the chart below, Vanguard shows the power of saving early in your career.

$1 could grow to much more by retirement—but it depends on when you start investing

The chart above assumes an annual 4% return after inflation and shows how a $1 contribu tion will compound if you give it time to grow. For example, if you contribute $1 at age 20 it could be $5.84 by the time you’re 65.

tion will compound if you give it time to grow. For example, if you contribute $1 at age 20 it could be $5.84 by the time you’re 65.

3. Go with a simple, low-cost investing plan

Robo-advisors are a new breed of low-cost automated investment platforms that use algorithms to manage portfolios efficiently and are offered online. Look for those that offer a balanced, diversified exposure with the ability to generate returns in all market cycles. Keeping fees to a minimum is especially important.

Chill out and worry about other things

You don’t need to check your account balance every day or constantly change your investment strategy based on the latest market rumor. If you save on a regular basis and invest in an appropriately diversified portfolio of stocks and bonds, you can put retirement worry aside and turn your attention to the other things in life, like how to spend your money when you retire as a millionaire.

***