Andrew Dassori, Chief Investment Officer & Co-CEO

Timothy Yan, Managing Director, Client Portfolio Management

The Federal Reserve’s anticipated cycle of interest rate hikes is now front and center for markets, and heightened anxiety among many investors has led to a widespread selling of financial assets. These dynamics have increased volatility to levels not seen since the onset of the COVID pandemic, and uncertainty over the trajectory for economic policy remains a key feature of the current environment.

In this research note, our goal is to provide a broader context for the dislocations that have resulted while assessing new risks and the broader opportunity set for investors to seek excess returns as markets recalibrate.

The beginning of 2022 featured an abrupt market transition driven by a shift in expectations for central bank policies and the economy. These dynamics combined with rising geopolitical risks and a changing shape of the pandemic to create uncertainty, volatility, and widescale deleveraging across asset classes. While this environment resulted in short-term pain for many investors, the market shakeup has in turn created opportunities for systematic strategies that seek to monetize market dislocations through a framework balanced to potential outcomes for the economy.

Impact of Changing Policy Expectations

Key Takeaways

|

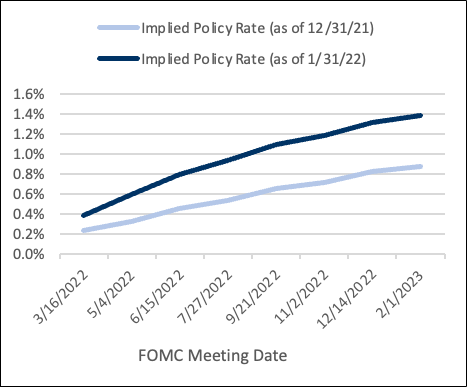

Figure 1: Futures Implied Policy Rate

Source: Bloomberg

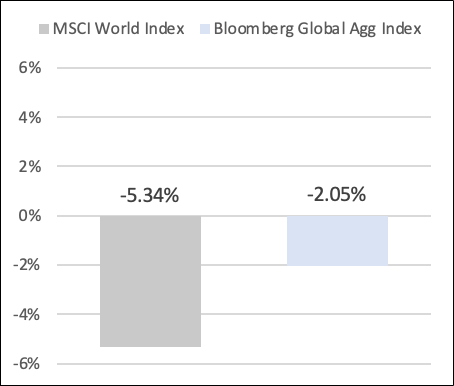

Figure 2: Stock & Bond Market Returns, Jan. 2022

Source: Bloomberg

The meaningful shift in the expected future path of interest rates highlighted above drove an uptick in volatility across markets. The ICE/BofA MOVE Index – which monitors the volatility of US Treasuries implied by options – reached its highest level since March 2020, and in this context both global stock and bond markets suffered losses. For the month of January 2022, the Bloomberg Global Agg and MSCI World Indices were down -2.1% and -5.3%, respectively, as a broad-based move out of financial assets left substantial market dislocations in its wake.

Trajectory of Returns After Prior Market Dislocations

|

Key Takeaways

Past performance does not guarantee future results and there is no assurance that the Fund will achieve its investment objective. |

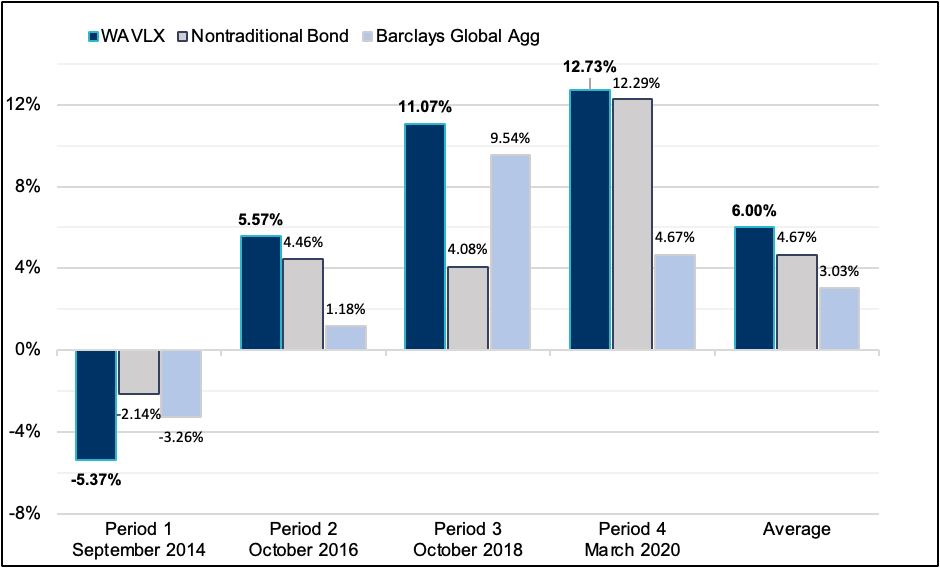

Figure 3: 12-Month Forward Returns Following Prior Market Dislocation Events

Source: Morningstar and Bloomberg, see notes for indexes & definitions

The set of outcomes following dislocation events is varied and features a wide range of underlying conditions that have driven returns. On the whole, however, markets have been resilient in the past, and we see no reason why they would not recalibrate to a new environment coming out of the recent turbulence. As the path for policy becomes clear and uncertainty subsides, we expect cash to broadly move back into markets based on the principle that investors naturally invest to outperform cash over the long-term.

|

Key Takeaways

|

The Federal Reserve will embark on its upcoming hiking cycle with the goal of balancing its mandate for stable prices with maintaining maximum employment and moderate long-term interest rates. An environment where inflation is at its highest level in decades creates a unique challenge for policymakers, and the risk of a policy error on either side is considerable.

In this context, we believe our approach is also differentiated in that we do not seek to forecast any specific economic conditions that result from these policies. We are instead positioned with a targeted balanced to growth and inflation, with a goal of maintaining an equal balance to potential outcomes for interest rates and the economy. In an environment of heightened uncertainty, we believe this is a prudent approach to investing that lets us attempt to limit exposure to large-scale directional risks and focus on monetizing the dislocations that may result from changing policy expectations across fixed income markets.

INDEXES:

Global stock market returns are represented by the MSCI World Index

Global bond market returns are represented by the Bloomberg Global-Aggregate Total Return Index

Nontraditional bond category is represented by the Morningstar Nontraditional Bond Category

TIME PERIOD DEFINITIONS:

Period 1 – September 2014

Period 2 – October 2016

Period 3 – October 2018

Period 4 – March 2020

DISCLAIMER:

Wavelength Capital Management, LLC (“Wavelength”) is an SEC-registered¹ investment adviser located in New York. Wavelength may only transact business in those states in which it is notice filed or qualifies for a corresponding exemption from such requirements. Wavelength's website is limited to the dissemination of general information regarding its investment advisory services to United States residents residing in states where providing such information is not prohibited by applicable law.

Accordingly, the publication of Wavelength's website on the Internet should not be construed as Wavelength's solicitation to effect, or attempt to effect, transactions in securities or the rendering of personalized investment advice for compensation over the Internet.

Investing involves the risk of loss and investors should be prepared to bear potential losses. Past performance may not be indicative of future results and may have been impacted by events and economic conditions that will not prevail in the future. No portion of this commentary is to be construed as a solicitation to buy or sell a security or the provision of personalized investment, tax or legal advice. Certain information contained in this report is derived from sources that Wavelength believes to be reliable; however, the Firm does not guarantee the accuracy or timeliness of such information and assumes no liability for any resulting damages.

For information pertaining to the registration status of Wavelength, please view the United States Securities and Exchange Commission’s website at www.adviserinfo.sec.gov. A copy of Wavelength's current written disclosure statement discussing Wavelength's business operations, services and fees is available from Wavelength upon written request. Wavelength does not make any representations as to the accuracy, timeliness, suitability, completeness or relevance of any information prepared by any unaffiliated third party, whether linked to Wavelength's website or incorporated herein, and takes no responsibility therefore. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

¹ SEC registration does not indicate a certain level of skill or training.

Financial professional use only. Do not distribute to the public.

Investors should carefully consider the investment objectives, risks, charges and expenses of the Fund before investing. To obtain a prospectus containing this and other important information, please call 1-866-896-9292 or visit www.wavelengthfunds.com to view or download a prospectus online. Read the prospectus carefully before you invest. There are risks involved with investing including the possible loss of principal. Past performance does not guarantee future results. Wavelength Funds are distributed by Ultimus Fund Distributors, LLC (Member FINRA). Wavelength Capital Management, LLC and Ultimus Fund Distributors, LLC are not affiliated entities.

Control Number: 14492655-UFD-02172022