“An oil prospector, moving to his heavenly reward, was met by St. Peter with bad news. ‘You’re qualified for residence,’ said St. Peter, ‘but, as you can see, the compound reserved for oil men is packed. There’s no way to squeeze you in.’ After thinking a moment, the prospector asked if he might say just four words to the present occupants. That seemed harmless to St. Peter, so the prospector cupped his hands and yelled, ‘Oil discovered in hell.’ Immediately the gate to the compound opened and all of the oil men marched out to head for the nether regions."

– Warren Buffet, re-telling a story from Benjamin Graham

Herd behavior has long been a staple in financial markets. Boom and bust cycles are widely observed, and this can create opportunities for disciplined momentum strategies. Simply chasing returns, however, has a high cost for investors.[1]

The growing popularity of venture capital is supported by tales of fantastic returns now sensationalized by pop culture and TV. While The Social Network and Shark Tank have made a positive impact by encouraging entrepreneurship and innovation, they have been less effective at setting investor expectations. Herein lies the risk. Increased flows to a space with low transparency and distinctly limited opportunities can be the classic setup for a bubble; in venture capital this is magnified by the boom or bust nature of the companies themselves.

Public vs. Private Investments

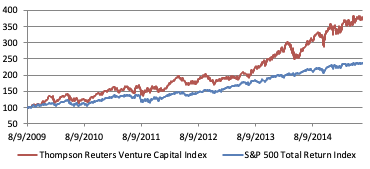

Figure 1: Thompson Reuters Venture Capital Index vs. S&P 500 Index

Source: Bloomberg LP

Holding all else equal, private investments are structured to reward investors with higher returns than those of public markets due to the premium paid for liquidity. The fact that it is more difficult to sell a private stake in a company is something investors should be compensated for, and this is evidenced in Figure 1. That being said, investors’ ability to allocate capital efficiently ultimately limits this experience when other opportunities become more attractive. Since ABC’s August 9, 2009 premiere of Shark Tank, the Thompson Reuters Venture Capital Index has risen over 280%, more than double the return of the S&P 500. With this outperformance, a crowd of investors has followed.

Returns alone are an inadequate measure of bubbles, but they offer a reasonable place to start. Knowing valuation metrics, such as price-to-book and price-to-earnings, are approaching cyclical highs for the S&P 500, one has to consider how these look for private companies which have been operating under the same economic conditions as their public counterparts.

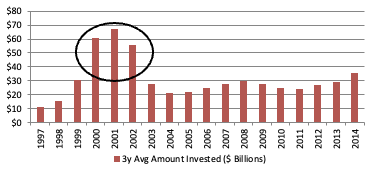

Figure 2: Rolling 3-Year Average Amount of Venture Capital Invested

Previous Bubble in VC Funding

Source: PricewaterhouseCoopers/National Venture Capital Association

Looking directly at venture capital funding, the most recent cycle provides useful context. In 1999, just before the bursting tech bubble caused venture capital to experience its worst returns on record, the 3-year average amount of venture capital invested crested just above $30 billion. As of year-end 2014, this measure was at its highest level in over a decade; more than $5 billion higher than it was in 1999.

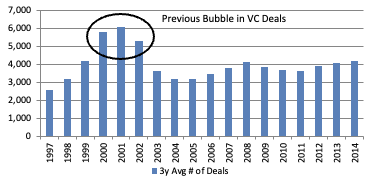

Figure 3: Rolling 3-Year Average Number of Venture Capital Deals

Source: PricewaterhouseCoopers/National Venture Capital Association

Similarly and as evidenced in Figure 3, the 3-year average number of venture capital deals is now at its highest level in 10 years, and also higher than it was in 1999. While technology, public policy, and other institutions continue to support innovation, there remains a limit to the supply of good ideas and, as a result, profitable venture capital deals.

For investors, it is important to recognize the value of venture capital investments and their impact of driving innovation in the global economy. At the same time it is important to understand their risks. Liquidity, transparency, and susceptibility to bubbles are among the key considerations for these markets, particularly during times of stress. While timing remains uncertain, whenever the bubble in venture capital does come to an end there will also be opportunities. Investors positioned strategically for where that capital flows are the ones who will benefit the most.

[1] Chien, YiLi (2014, April 14). “Chasing Returns Has a High Cost for Investors,” The Federal Reserve Bank of St. Louis: On the Economy

***