Companies are facing headwinds while at their most vulnerable point in decades

Mark Landis & Tim Yan

|

KEY TAKEAWAYS

|

The dislocations across fixed income witnessed so far this year are of a magnitude not seen in decades. Inflation has eclipsed double digits in many parts of the globe for the first time in nearly 40 years[1], and the policy response has been painful for portfolios. In the US, the Federal Reserve is making up for falling behind the curve by raising rates at the fastest pace since the 1980s which has helped propel the dollar to its strongest levels this century. These policy dynamics have spread far beyond our borders, as governments and central banks scramble to bring order back to their economies.

Despite their best efforts, global equities have dropped by more than 25%[2], and government bond markets are on pace for their worst year since 1949. Alongside $40 TN of losses in capital markets, there is a nauseating sense that this may be just the beginning and there could be more pain to come. High yield credit is down over 12% YTD[3], yet the yield premium remains below the average spreads of the last 20 years - where they’ve been for much of the past decade, albeit for a brief 3-month pandemic-induced blowout[4] (Figure 1).

Figure 1: ICE BofA US High Yield Option-Adjusted Spread

Source: Federal Reserve Bank of St. Louis

Default rates have thus far managed to remain relatively low with little sign of picking up soon. With negativity and recession fears increasing, one of the most common questions we’ve been asked by investors is, “given the decline in markets, why aren’t more companies struggling, and why haven’t we seen defaults rise as fast as one might expect?”

While our investment process does not attempt to time or make directional bets on credit or interest rates, our research suggests that the delay in the rise of defaults may be due to a fiscal overhang from the pandemic-related stimulus that led to corporate cash reaching never before seen levels[5] amidst a prolonged low interest rate environment. As this pandemic-era largesse works its way through the system, however, there is a real fear that we may see the inevitable rise in defaults late next year and into 2024.

There’s No Such Thing as a Free Lunch

In response to the COVID-19 pandemic, central banks across the globe rushed to cut interest rates to help support underlying economies. In response, companies jumped at the opportunity to refinance their higher-cost obligations and raise cash, increasing overall liquidity and resulting in record levels of corporate issuance in 2020 and 2021 (Figure 2).

Figure 2: US Investment Grade and High Yield Corporate Issuance, in $Billions

Source: Securities Industry and Financial Markets Association

It is not surprising that once the Fed started raising rates in 2022, investment-grade corporate debt issuance declined significantly in the first half compared to the previous year. High yield issuance fell almost 74% across that time period and is down 61% from the first half of 2020, with 2022 on pace to be the lowest since 2008.[6]

Kicking the Can Down the Road

Since the Great Recession[7], companies have been able to access increasingly cheap credit, and many took this to extreme levels by piling on so much debt that it put them on the verge of junk status. For most of these less frequent issuers which make up much of the high yield market, pressure to refinance this debt will come in the next couple of years. According to Deutsche Bank, there is around $11 BN in high yield bonds coming due through the end of the year, followed by approximately $62 BN and $107 BN in 2023 and 2024, respectively. If you take into consideration loans and revolving-credit facilities, speculative companies have maturities of around $1.47 TN through 2027.[8]

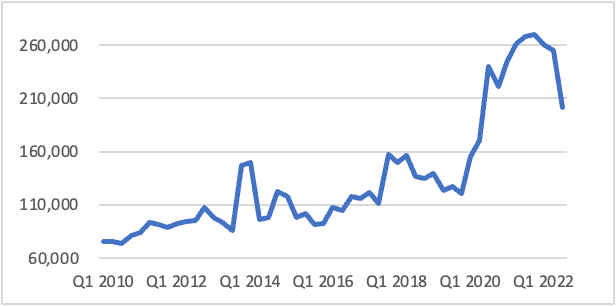

This pressure to refinance couldn’t come at a worse time for companies. Third-quarter earnings have already shown that they have not been immune to the effects of a slowing economy, and adding high inflation and increased borrowing costs to the equation has forced companies to draw down on cash levels since the start of the year (Figure 3). It’s worth noting that since corporations had built up such high cash levels throughout the pandemic, the drawdowns that we’ve seen thus far could be viewed as bringing them back in line with more normal historical levels, but if this trend continues the financial situation for these companies could become increasingly concerning.

Figure 3: US Corporations Total Cash on Hand and in US Banks, in $Millions

Source: Federal Reserve Bank of St. Louis

All Good Things Must Come to an End

Nothing lasts forever, and eventually, companies will be forced to make difficult decisions as their cash levels deteriorate. If the Fed continues on its current path of raising rates in an attempt to bring down inflation, companies will face the inevitable question of what to do about the mountains of debt that they have amassed in recent decades. If interest rates continue to rise and the global economic slowdown deepens, weaker speculative grade companies will confront declining growth and earnings at the very same time that their debt servicing costs escalate. This would exacerbate the decline of their cash levels and increase refinancing costs that are coming due over the next few years. In that scenario, we would expect defaults to rise, affecting the most vulnerable companies first and putting further stress on the rest of the market.

Nobody has a crystal ball, and while it may seem obvious that current corporate debt levels in need of servicing are unsustainable, it is much harder to time precisely when and where one might see the first cracks. We contend that a more practical approach to building investment portfolios involves balancing risk across potential economic outcomes and how they may impact fixed income markets as interest rate and credit cycles turn. In this process, we seek to insulate portfolios from the day-to-day noise of others trying to predict the future while focusing on the current opportunity set and preparing for what can come next in markets and the economy.

[1] Financial Times, Global inflation tracker: see how your country compares on rising prices

[2] MSCI ACWI Index, YTD as of Sept. 30, 2022

[3] ICE BoA US High Yield Index, YTD as of Sept. 30, 2022

[4] Federal Reserve Bank of St. Louis, ICE BofA US High Yield Option-Adjusted Spread

[5] Federal Reserve Bank of St. Louis, Quarterly Financial Report: U.S. Corporations: Total Cash on Hand and in US Banks

[6] Securities Industry and Financial Markets Association (SIFMA), US Corporate Bond Statistics, Issuance

[7] Great Recession: December 2007-June 2009

[8] Wall Street Journal, Junk-Rate Companies Search for the Right Time to Tap Investors

Index Definitions:

MSCI ACWI Index is designed to represent the performance of the full opportunity set of large and mid-cap stocks across 23 developed and 24 emerging markets.

The ICE BofA Option-Adjusted Spreads (OASs) are the calculated spreads between a computed OAS index of all bonds in a given rating category and a spot Treasury curve.

The ICE BofA US High Yield Index tracks the performance of US dollar denominated below investment grade rated corporate debt publicly issued in the US domestic market

The Securities Industry and Financial Markets Association is a United States industry trade group representing securities firms, banks and asset management companies.

Disclaimer:

Wavelength Capital Management, LLC (“Wavelength”) is an SEC-registered¹ investment adviser located in Connecticut. Wavelength may only transact business in those states in which it is notice filed or qualifies for a corresponding exemption from such requirements. Wavelength's website is limited to the dissemination of general information regarding its investment advisory services to United States residents residing in states where providing such information is not prohibited by applicable law. Accordingly, the publication of Wavelength's website on the Internet should not be construed as Wavelength's solicitation to effect, or attempt to effect, transactions in securities or the rendering of personalized investment advice for compensation over the Internet. Investing involves the risk of loss and investors should be prepared to bear potential losses. Past performance may not be indicative of future results and may have been impacted by events and economic conditions that will not prevail in the future. No portion of this commentary is to be construed as a solicitation to buy or sell a security or the provision of personalized investment, tax or legal advice. Certain information contained in this report is derived from sources that Wavelength believes to be reliable; however, the Firm does not guarantee the accuracy or timeliness of such information and assumes no liability for any resulting damages. For information pertaining to the registration status of Wavelength, please view the United States Securities and Exchange Commission’s website at www.adviserinfo.sec.gov. A copy of Wavelength's current written disclosure statement discussing Wavelength's business operations, services and fees is available from Wavelength upon written request. Wavelength does not make any representations as to the accuracy, timeliness, suitability, completeness or relevance of any information prepared by any unaffiliated third party, whether linked to Wavelength's website or incorporated herein, and takes no responsibility therefore. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

¹ SEC registration does not indicate a certain level of skill or training

Control Number: 16022246-UFD-11212022